Beware the Volatility Thief

One of the most misunderstood ideas in investing is what volatility is. Even less well understood is what volatility does. High volatility does not just force you to take a wilder ride; higher volatility, all else equal, actually reduces the returns you think you get. That’s why very diversified and lower volatility investments (think broad market ETFs and index funds) deliver more investment bang for the buck than you might think, and why individual stocks deliver less. Volatility is a return thief.

First, let’s define the terms. Suppose we want to talk about the S&P 500 Index. If you go online you can find historical returns for the S&P 500 at New York University’s Stern School of Business here: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html. Not only can you look at it, but you can download the data to a spreadsheet.

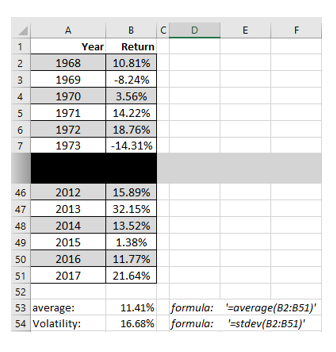

If you do that, you will see that over the past 50 years – from 1968 to 2017 – the average return of the S&P 500 was 11.41%. But it isn’t a steady 11.41%; it jumps around – which is what we mean by volatility:

Now, the usual definition of volatility is standard deviation. If you wanted to get the numbers yourself, you would likely calculate it by pasting the data in a spreadsheet and taking the average and standard deviation like so, using the spreadsheet’s tools (I have squeezed down a bunch of the intervening years to save space):

So far, so good. We have calculated that the average return and the volatility are 11.41% and 16.68%, respectively. Or at least we think so.

But we haven’t done it quite right.

To see things go astray, suppose, instead, someone had offered investors a “bond” at the start of 1968 that would pay 11.41% every year for the next 50 years (and let’s make it a zero-coupon bond that pays out nothing along the way that would need reinvesting; like a savings account, such a bond would keep appreciating in value by 11.41% every year, and pay the total all out at the end).

Let’s see what you would end up with if you took this hypothetical bond paying a steady 11.41% and compared that to what happened if you had actually invested $100 in the stock market over the same period. Since we know the market averaged 11.41%, you might think we would end up with the same amount, right?

No. If you looked in the two accounts, here is what that $100 turned into with the two different, but seemingly identical, investments:

Hypothetical Bond: $22,146

Actual S&P 500: $11,995

Now of course, no one really offered such a bond in 1968. But our intuition – and the way a lot of people calculate returns via a spreadsheet – makes most people believe these should have given the same result. But the stock market came in at half the final balance.

Why did this happen? Since we are doing this all after-the-fact, the problem can’t be the market had a bad year (or bad years) that we failed to forecast. After all, we designed the mythical bond to have the same return the market did after we knew what the market had already done. So what happened here?

The volatility thief struck.

Here is what most people miss. The hypothetical bond had zero volatility and paid exactly 11.41% per year. That pattern – equal returns every year – gives the highest actual return of any other set of returns that average to 11.41%; all others with the same average will be lower, and the higher the volatility the lower the outcome. That is the volatility thief.

To see why this is true, let’s suppose the market didn’t deliver 11.41% annually, but alternated between 12.41% and 10.41% every two-year cycle – that’s 1% above and below 11.41%, so it averages out to 11.41%. And let’s look at the first two years of these two investments:

| End of Year… | Amount in Bond | Bond return | Amount in Stock | Stock Return | |

| 0 | $100 | 11.41% ($11.41) | $100 | 12.41% ($12.41) | |

| 1 | $111.41 | 11.41% ($12.71) | 112.41 | 10.41% (11.24) | |

| 2 | $124.12 | $123.65 |

Even though these two investments had the same average return over the two years, the stock – which had a tiny amount of volatility – came up $0.77 short. That’s not much. But don’t forget, we also assumed very low volatility; the real stock market had a volatility of about 17% over this period. That’s how $11,000 of apparent returns disappeared. That is the volatility thief at work.

In this case, the volatility led to an actual (and properly calculated) annualized return of the stock market of only 10.05% over this period – i.e., that is the amount that, if earned exactly every year would have delivered the what a real investor would have gotten from stock. It’s only 1.36% lower than the average return, but over 50 years that eats into half the returns you might have thought you would get.

All of this is simply a matter of arithmetic that is often overlooked: If you calculate numbers on a spreadsheet as we did above, with volatility you don’t get the average return you calculated, you get less – and how much less grows as volatility is increased. In fact, here is a table of what an investment whose annual returns average out to 10% actually becomes at different levels of volatility:

| Volatility | Starting Value | Value After 10 Years | Actual Annual Return |

| 0% | $100 | $673 | 10.0% |

| 10% | $100 | $618 | 9.5% |

| 20% | $100 | $435 | 8.0% |

| 30% | $100 | 38 | -4.7% |

As you can see, increasing volatility makes the actual returns very different from the apparent average returns. With enough volatility they can become negative.

I see four takeaways from this for investors:

- Volatility, as defined here, is a thief. As volatility goes up, actual realized returns drop below the average you might calculate on a spreadsheet for any investment. In fact, if volatility gets large enough, it is entirely possible to have positive average returns but actually lose money – i.e., suffer negative actual returns. When you consider that some single stocks and high-octane strategies might have 40% or greater volatility, that matters.

- A 1% difference in returns adds up over time. In this case, a difference of 1.36% halved the apparent returns. But it doesn’t matter where that 1% came from – volatility impact, management fees, or tax inefficiency. In the long run, giving up 1% to any factor, or combination, could take away half your wealth.

- The biggest takeaway? Low-cost, broadly diversified, tax-efficient, and relatively low volatility ETFs and index funds deliver more return than you think relative to other investments. People chasing returns from higher volatility investments take on a risk of doing poorly they usually underestimate terribly.

That’s what makes ETFs and index funds such good building blocks.